EXPANSION OF THE URBAN

TRANSIT AREA INTO NEW

DEVELOPING AREAS DOCUMENT

1

|

1. transit levy policy review examen de la politique

concernant la taxe sur le transport en commun |

report recommendations

That Council approve:

1. The revisions to the boundary of the Urban Transit Area detailed in this report to be effective on January 1, 2009, to provide for the provision and funding of transit service in expanding areas of the city;

2. The strategy detailed in this report to complete the transition of Stittsville into the Urban Transit Area over the years 2009 to 2011; and,

3. The re-allocation of maintenance costs for park and ride lots, as detailed in this report, so that the costs are shared equally by all city taxpayers.

recommandations du rapport

Que Conseil approuve:

1. les modifications des

limites du secteur de transport en commun urbain décrites dans le présent

rapport et mises en vigueur le 1er janvier 2009, afin d’assurer

la prestation et le financement des services de transport en commun dans les

nouveaux quartiers de la ville;

2. la stratégie expliquée

dans le présent rapport visant à assurer l’intégration de Stittsville au

secteur de transport en commun urbain sur la période allant de 2009 à 2011;

3. la nouvelle distribution

des coûts d’entretien des parc-o-bus, comme l’explique le présent rapport, afin

que les frais soient également répartis entre tous les contribuables de la

ville.

Documentation

1. Deputy

City Manager’s report (Planning, Transit and the Environment) dated 31 October

2008 (ACS2008-ICS-TRA-0018).

2. Extract

of Draft Minute, 10 November 2008, to be distributed prior to Council Meeting.

Report to/Rapport au

:

Transit Committee

Comité du

transport en commun

and

Council / et au Conseil

31

October 2008 / le 31 octobre 2008

Submitted by/Soumis par: Nancy Schepers, Deputy City

Manager/Directrice municipale adjointe

Infrastructure Services and Community Sustainability/Services d’infrastructure

et Viabilité des collectivités

Contact Person/Personne

ressource : Alain Mercier, Director/Directeur

Transit Services/Services du transport en commun

613-842-3636 x2271, Alain.Mercier@ottawa.ca

|

Ref N°: ACS2008-ICS-TRA-0018 |

|

SUBJECT: |

|

|

|

|

|

OBJET : |

examen de LA POLITIQUE CONCERNANT LA TAXE SUR LE TRANSPORT EN COMMUN |

REPORT RECOMMENDATIONS

That the Transit Committee recommend Council approve:

1. The revisions to the boundary of the Urban Transit Area detailed in this report to be effective on January 1, 2009, to provide for the provision and funding of transit service in expanding areas of the city;

2. The strategy detailed in this report to complete the transition of Stittsville into the Urban Transit Area over the years 2009 to 2011; and,

3. The re-allocation of maintenance costs for park and ride lots, as detailed in this report, so that the costs are shared equally by all city taxpayers.

RECOMMANDATIONS DU RAPPORT

Que le Comité du transport en commun recommande au

Conseil d’approuver :

1. les modifications des limites du secteur de transport en

commun urbain décrites dans le présent rapport et mises en vigueur le 1er

janvier 2009, afin d’assurer la prestation et le financement des services

de transport en commun dans les nouveaux quartiers de la ville;

2. la stratégie expliquée

dans le présent rapport visant à assurer l’intégration de Stittsville au

secteur de transport en commun urbain sur la période allant de 2009 à 2011;

3. la nouvelle distribution

des coûts d’entretien des parc-o-bus, comme l’explique le présent rapport, afin

que les frais soient également répartis entre tous les contribuables de la

ville.

BACKGROUND

In June and July 2005, Transportation Committee and Council considered a staff report with recommendations to change the area over which property taxes are collected to fund the net capital and operating costs of the transit system (Urban Transit Area Review, at Transportation Committee, June 15, 2005, and at Council, July 13 to 15, 2005).

The staff report recommended expanding the Urban Transit Area (UTA) to include all of Stittsville and Kanata West and certain parts of South Nepean and South Gloucester, to phase-in the full transit tax rate over four years, and to improve service to those new areas to conform with the service standards applied in the current Urban Transit Area.

Council did not approve those recommendations, but instead established a new Town Transit Area for Stittsville, so that property taxes collected in Stittsville would fund the net operating costs of transit service in Stittsville and would contribute to the net capital costs at the same rate as in the UTA. Council approved as follows:

-

That a Town Transit Area (TTA) be created that aligns with the urban

boundary of Stittsville;

-

That a Town Transit tax levy be introduced to ensure that the taxpayers

of Stittsville pay the full net costs of the transit services their community

receives;

-

That the Town Transit tax levy include the same capital contribution as

the UTA levy;

-

That the TTA and Town Transit Levy be introduced in 2006;

-

That every three years, starting in September 2005, OC Transpo carry

out a Town Transit Review, modeled on its highly successful 2001 Rural Transit

Review, during which staff work in close collaboration with ward councillors,

residents and business owners to evaluate the changing transit needs of

communities within the TTA and formulate recommendations for City Council to

meet those needs and cover the costs.

Following from this decision, service levels in Stittsville have been increased, but not as much as to comply with the UTA service standards, and property taxes collected in Stittsville to fund transit are higher than previously, but not as high as in the UTA (in 2007, for a typical residential property, $306 in Stittsville and $486 in the UTA).

At its meetings of December 3 to 12, 2007, Council considered the following motion and referred it to Transit Committee:

WHEREAS Council approved in July 2005 that the Transit Tax be reviewed every 3 years;

AND WHEREAS the last review

of the tax areas was undertaken in 2005;

AND WHEREAS the cost of the

construction of Park ‘n Rides should be borne city-wide in consideration of the

usage of rural residents of our Park ‘n Ride system;

THEREFORE BE IT RESOLVED

THAT the capital cost of Park ‘n Rides be distributed equally across the Urban,

RTA A, RTA B and TTA effective on the 2008 tax bill;

AND BE IT FURTHER RESOLVED

THAT staff undertake a review of the Transit tax with the aim of bringing new

communities into the UTA and eliminating the TTA;

AND BE IT FURTHER RESOLVED

THAT this review be undertaken and implemented prior to the setting of the 2008

tax rate.

A

report responding to this direction was presented to Transit Committee at its

meeting of March 19, 2008. At that

meeting, the Committee referred the report back to staff, with the following

direction:

BE IT HEREBY RESOLVED that the Rural Transit Levy report be referred back to staff to report back to Transit Committee by the fall of 2008;

AND THAT staff be directed to undertake consultation with ward

councillors, residents and business owners on the recommendations in this

report and develop recommendations on the amount and phase-in of any increase

in levies at a Transit Committee meeting in September/October with the first

stage of any increases in levies, once approved by City Council, to form part

of the 2009 budget.

This report responds to both the motions from December 3 to 12, 2007, and March 19, 2008.

DISCUSSION

Current Transit Levies

Property taxes to fund the net capital and operating costs of transit service are now collected at different rates in four different areas, and different service standards apply in these areas:

· Urban Transit Area (UTA) – The UTA extends from Kanata to Orléans and from the Ottawa River to Barrhaven, Riverside South, and Leitrim. It is generally the developed part of the Urban Area (as defined in Schedule B of the Official Plan), with the exception of some areas, which were developed before the urbanized part of the city grew to approach them. Service is provided to bring 95 per cent of the population within a five-minute walk of transit service in peak periods and within a ten-minute walk at other times of the day. Taxes are collected to cover the net operating costs of transit service provided in the UTA (total operating costs less fare revenue) and to cover the net capital costs of transit equipment and infrastructure (total capital costs less contributions from other levels of government). In 2007, the UTA levy for a typical residential property assessed at $279,000 was $486.

· Town Transit Area (TTA) – The TTA covers the boundaries of the village of Stittsville (defined as the part of the Urban Area that was in the former Township of Goulbourn). Stittsville is the largest of the developed parts of the Urban Area that is not part of the UTA. Service is provided at levels that were adopted following public consultation in 2006. Peak-period service is provided within a five-minute walk of most of the area, and all-day service is provided within a 20-minute walk of most of the area. Fares for direct-to-downtown express service are higher than they are in the UTA. Taxes are collected to cover the net operating costs of transit service in Stittsville and to cover the capital costs for the transit system at the same rate as in the UTA. In 2007, the TTA levy for a typical residential property assessed at $279,000 was $306.

· Rural Transit Area A (RTA-A) – RTA-A is a ring around the urbanized part of the city, including most of the villages that are closest to the urbanized part of the city. RTA-A includes Richmond and most of Goulbourn; North Gower and Manotick and the eastern half of Rideau; all of non-urban Nepean; Carlsbad Springs and all of non-urban Gloucester; and Cumberland Village, Navan, Sarsfield, and Vars, and all of non-urban Cumberland. Service is provided in peak periods only, generally with two or three morning trips and two or three afternoon trips. Fares for direct-to-downtown express service are higher than they are in the UTA, and are the same as in the TTA. Taxes are collected to cover the net operating costs of transit service in RTA-A and to cover the net capital costs of the transit equipment that is used to provide service in RTA-A. In 2007, the RTA-A levy for a typical residential property assessed at $279,000 was $96.

· Rural Transit Area B (RTA-B) – RTA-B is the outer ring around RTA-A. RTA-B is made up of all parts of the city that are not within the other three areas. RTA-B includes all of West Carleton and non-urban Kanata, the very western part of Goulbourn, the western half of Rideau, and all of Osgoode. No conventional transit service is provided by the City in RTA-B. Some commuter services are provided by independent bus companies, with no financial contributions from the City. The City provides Para Transpo for qualifying people with disabilities. Taxes are collected to cover the net costs of Para Transpo service (pooled with RTA-A). In 2007, the RTA-B levy for a typical residential property assessed at $279,000 was $26.

Expanding

the Urban Transit Area

The Urban Transit Area (UTA), defined by by-law, sets out the area within which regular transit service is provided and within which a tax levy to contribute to the costs of transit service is applied. The UTA encompasses the central, urban parts of the city, generally from Kanata to Orléans and as far south as South Nepean and Riverside South. Council and the former Regional Council have approved revisions to the boundary of the UTA from time to time to keep pace with the growth of the urban area.

At its meeting of July 11, 2001, Council approved a

report entitled Financing Methods – Funding City Services, which

directed that “properties . . . be automatically included in the Urban Transit

Area as they receive the defined level of transit service.” Staff identify the areas to be added to the

UTA through the normal development approval and transit planning processes, but

the by-law to define the UTA needs to be approved by Council.

The boundaries of the UTA were last updated in 2006

following the approval of a report approved by Council at its meeting of

October 19, 2005. Since that time, new

urban development has been approved and is now under construction. These new areas will receive transit service

as they are built and need to be added to the UTA so that they share in the

funding of the cost of building and operating the transit system.

Since the boundaries of the Urban Transit Area were

last updated in 2006, development has been approved in six areas. These areas are recommended for addition to

the UTA starting on January 1, 2009, and are shown on the map in Document

1, attached.

The six areas are:

· New parts of Kanata Lakes and Kanata North

· The Fernbank lands between Kanata and Stittsville

· New parts of Barrhaven west of Cedarview and south of Strandherd

· A new subdivision of Riverside South west of River Road

· A new part of Leitrim east of Bank Street

· The East Urban Community lands near Renaud Road and Mer Bleue Road

Continuing the Transition of

Stittsville into the Urban Transit Area

Following the direction of Council in 2005 to re-examine the transit needs of Stittsville every three years, and based on the analysis and consultation described below, staff recommend that the transition of Stittsville into the Urban Transit Area continue, with service increases and accompanying tax rate increases in the years 2009, 2010, and 2011. These would be the final three years of a ten-year phase-in of urban transit service.

This strategy would provide for:

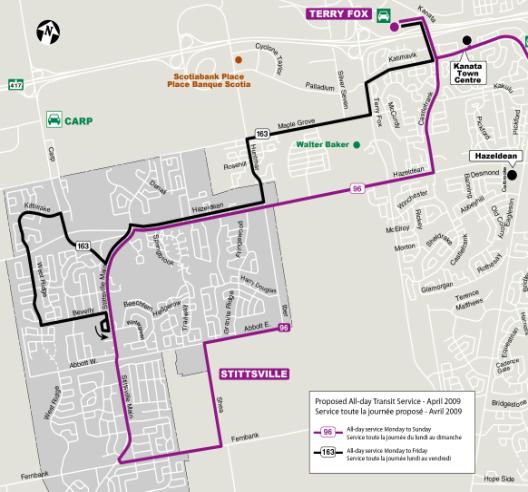

· A new local route, operating seven days week, every 30 minutes, to bring more residents within a ten-minute walk of all-day service (to start from Monday to Friday in April 2009, and to operate all week long from September 2010);

· A service increase to 30-minute service on Route 96 on Sundays (to start in April 2009);

· Two more morning trips and two more afternoon trips on Stittsville express routes (afternoon trips to be added in April 2009 and morning trips to be added in September 2010); and,

· Lower fares on Stittsville express routes 261, 262, and 263 so that they would be the same as on express routes in the UTA (to begin in July 2010).

Currently, transit service in Stittsville is at approximately two-thirds of the level that would be provided if the service standards of the Urban Transit Area were applied. With the recommended strategy, both the tax rate and the level of service would rise to approximately 80 per cent in 2009, 90 per cent in 2010, and 100 per cent in 2011. From 2011, Stittsville would be part of the UTA for all purposes, and the Town Transit Area would no longer exist as a distinct taxation area.

Staff presented this strategy and the proposals for transit route changes at a public meeting on October 7, 2008, organized by Councillor Qadri. If Council approves the strategy in this report and the funding in the 2009 operating budget, staff will continue to work with Councillor Qadri and his office in reaching a community consensus on the details of the service changes, with an aim to implement the changes in April 2009. Staff will report the agreement to Transit Committee, in the same way as is done for Transplan service change proposals in the UTA.

Funding the Maintenance Costs of Park and Ride Service City-Wide

Staff recommend that the maintenance costs for the City’s park and ride lots be shared equally across all property taxpayers, rather than just those inside the Urban Transit Area. This recommendation is to more-equitably share the costs of the service.

Currently, the park and ride lots are used 64 per cent by customers living inside the UTA, 15 per cent by customers living in other parts of the city, and 21 per cent by customers living outside the city. Detailed figures on park and ride use are shown in the table in Document 3, attached.

There is no mechanism for the City to recoup the costs that are borne on behalf of transit customers who live outside the City of Ottawa. Staff have identified no way of charging individual customers for their use of the park and ride lots that would not impose so much inconvenience on customers – both those from inside and outside the city – that the result would be reduced transit ridership (see Document 7 for discussion of this topic). There are benefits for city residents and taxpayers of having customers from outside the city use transit, and those benefits are consistent with providing a municipal subsidy for those customers.

Maintenance costs for the park and ride lots are approximately $1.2 million in 2008. This amounts to $3.44 in property taxes (for a typical residential property assessed at $279,000) inside the UTA. With the staff recommendation, the funding would be spread more widely, and would amount to $3.06 in property taxes for all city taxpayers. This would be a reduction of 38 cents per year for properties inside the UTA and an increase of $3.06 per year for properties in other parts of the city. With this change (and not reflecting the recommendation for increased service in Stittsville), the tax amounts would be approximately $486 in the Urban Transit Area, $309 in the Stittsville Town Transit Area, $99 in Rural Transit Area A, and $29 in Rural Transit Area B.

With the staff recommendation, 89 per cent of the maintenance costs would be paid from property taxes collected in the UTA and 11 per cent would be paid from property taxes collected in other parts of the city. The operating costs of the transit services from the park and ride lots would continue to be funded by customers’ fares and by property taxes collected in the UTA.

Staff are making no recommendation at this time regarding the funding of park and ride capital costs. No new park and ride projects are planned in the 2009 capital budget. Recommendations for funding the future rapid transit network, including future park and ride lots, will be made separately.

RURAL IMPLICATIONS

The expansion of the Urban Transit Area and the strategy for the continued transition of Stittsville into the UTA have no effect on the rural parts of the city.

The recommendation to share funding of the maintenance costs for park and ride lots equally across the city would increase property taxes in rural areas by $3.06 per year for a residential property assessed at $279,000.

CONSULTATION

The recommended expansion of the Urban Transit Area follows long-standing Council direction and was the subject of no specific consultation. Consultation on expanding transit service into developing areas is conducted through the normal Transplan consultation process, as described in the Transit System Management Policies report, approved by Council at its meeting of June 22, 2005.

The recommended strategy to continue the phased introduction of

Stittsville into the Urban Transit Area was presented by staff to a community

meeting organized by Councillor Qadri on October 7, 2008.

FINANCIAL IMPLICATIONS

The expansion of the Urban Transit Area has no immediate financial implications. Rather, it increases the number of properties over which the net costs of operating transit service are shared. Any operating cost increases to serve the new areas of the UTA would be part of the transit operating budgets as submitted for 2009 and subsequent years.

The recommended increase in transit service in Stittsville has a net cost of approximately $380,000 in 2009. This amount is subject to approval by Council in the 2009 transit operating budget.

The recommendation to share

funding of the maintenance costs for park and ride lots equally across the city

has no financial implications. The

costs would remain unchanged, but they would be funded by a different

distribution of property taxes across the city.

SUPPORTING DOCUMENTATION

Document 1 Expansion of the Urban Transit Area into New Developing Areas

Document 2 Transit Levy and Transit Service in Stittsville

Document 3 Park and Ride Use by Area, April to May 2008

Document 4 Stittsville Town Transit Area

Document 5 Rural Transit Areas A and B

Document 6 Changes in Tax Rates with City-wide Sharing of Park and Ride Maintenance Costs

Document 7 Methods to Charge Additional Fees for Park and Ride Users from Outside Ottawa

DISPOSITION

Upon approval of Recommendation 1 of this report, to expand the Urban

Transit Area, a by-law will be prepared for enactment at a subsequent meeting

of Council. That by-law will replace

the current by-law.

Upon approval of Recommendation 2 of this report, the strategy to

continue the phased introduction of Stittsville into the Urban Transit Area,

and subject to the approval of funds in the 2009 transit operating budget,

staff would continue to work with Councillor Qadri and his office in reaching a

community consensus on the details of the service changes, with an aim to

implement the changes in April 2009.

Upon approval of Recommendation 3 of this report, to share funding of the maintenance costs for park and ride lots equally across the city, staff would make the appropriate changes to tax rates for 2009.

EXPANSION OF THE URBAN

TRANSIT AREA INTO NEW

DEVELOPING AREAS DOCUMENT

1

TRANSIT LEVY AND

TRANSIT SERVICE IN STITTSVILLE DOCUMENT 2

In 2005, Council established the new Town Transit Area (TTA) to isolate the costs of providing transit service in Stittsville and to ensure that property taxes collected in Stittsville would cover the net capital and net operating costs of the transit services provided there.

In 2006, following an extensive process of consultation with transit customers and residents of Stittsville, transit service was improved in several ways:

· Route 96 was extended into residential and employment areas in the southeastern part of Stittsville;

· Route 96 was increased to 30-minute service at most times from Monday to Saturday;

· New Sunday service was introduced on Route 96, every 60 minutes;

· A new Route 261 was introduced, replacing the eastern part of the previous Route 262; the route operates with four new morning trips and four new afternoon trips; and,

· Route 262 was extended to serve new residential areas in the southern part of Stittsville; the service was increased from four to six morning trips and from four to six afternoon trips.

With these improvements, the service that is provided in Stittsville is approximately two-thirds of the level of service that would be provided if the Urban Transit Area service standards were applied there. There remain times of the week when the base route operates every 60 minutes instead of every 30 minutes, there remain substantial areas of Stittsville, which are beyond a 10‑minute walk of all-day transit service, and there continues to be a higher fare charged on the express routes than is charged in the UTA.

Transit ridership to and from Stittsville has increased greatly over the past several years, both following and leading the service improvements before 2006 and those described above. In 2002, transit ridership to or from Stittsville (including Stittsville residents’ use of park and ride lots in Kanata) was 207,000. In 2008, ridership is on-track to be 573,000, almost three times the 2002 level. Clearly, Stittsville residents are recognising and making use of the value of public transit service.

In 2007, the TTA levy for a residential property assessed at $279,000 was $306. This is 63 per cent of the $486 that was collected in the Urban Transit Area for a residential property with similar assessment.

Property taxes collected in Stittsville do not contribute to the costs of service provided from the park and ride lots, though approximately 108,000 customer-trips are made to or from the park and ride lots in Kanata by residents of Stittsville. The costs to provide that service are paid entirely from property taxes collected in the UTA.

If Stittsville were part of the UTA and the same service standards were applied there as in the rest of the UTA, the following changes would be justified:

· A new local route, operating seven days week, every 30 minutes, to bring more residents within a ten-minute walk of all-day service;

· A service increase to 30-minute service on Route 96 on Sundays;

· Two more morning trips and two more afternoon trips on Stittsville express routes; and,

· Lower fares on Routes 261, 262, and 263 so that they would be the same as on express routes in the UTA.

The net operating cost of these changes would be $1.44-million in a full year. Because some of the changes would be introduced in April 2009 and others in July and September 2010, the costs would be phased-in over the years from 2009 to 2011.

With these changes, Stittsville would from 2011 have the same tax rates and transit service planned under the same service standards as the rest of the UTA. From 2011 on, transit services in Stittsville would be funded and planned along with those in the rest of the UTA, and the TTA would no longer exist as a distinct taxation area.

Proposed

revisions to all-day transit service for April 2009

PARK AND RIDE

USE BY AREA, APRIL-MAY 2008 DOCUMENT 3

|

Lot |

Spaces Used |

Capacity |

Home location of customers |

|||

|

Urban Transit Area |

Stittsville |

Rural Areas |

Outside Ottawa |

|||

|

Baseline |

240 |

276 |

93% |

– |

3% |

4% |

|

Eagleson |

1242 |

1184(1) |

47% |

15% |

17% |

21% |

|

Fallowfield |

1017 |

1002(2) |

80% |

– |

8% |

12% |

|

Greenboro |

667 |

678 |

68% |

– |

9% |

23% |

|

Place

d’Orléans |

557 |

568 |

67% |

– |

4% |

29% |

|

Strandherd |

96 |

336 |

69% |

1% |

14% |

16% |

|

Terry

Fox |

140 |

515 |

24% |

20% |

28% |

28% |

|

Trim |

443 |

641 |

57% |

– |

6% |

37% |

Small lots(3)

|

62 |

140 |

74% |

– |

– |

26% |

Total/overall

|

4464 |

5340 |

64% |

5% |

10% |

21% |

Notes:

1. Eagleson capacity expands to 1217 outside the winter months

2. Fallowfield capacity expanded to 1025 since survey conducted

3. Three small urban lots aggregated: Blair, Jeanne d’Arc, and Riverview

Sources:

- Park and ride lot counts, April 2008

- Home

locations from Gold Permit holder records, May 2008

- Home locations from MTO licence plate records, May 2008

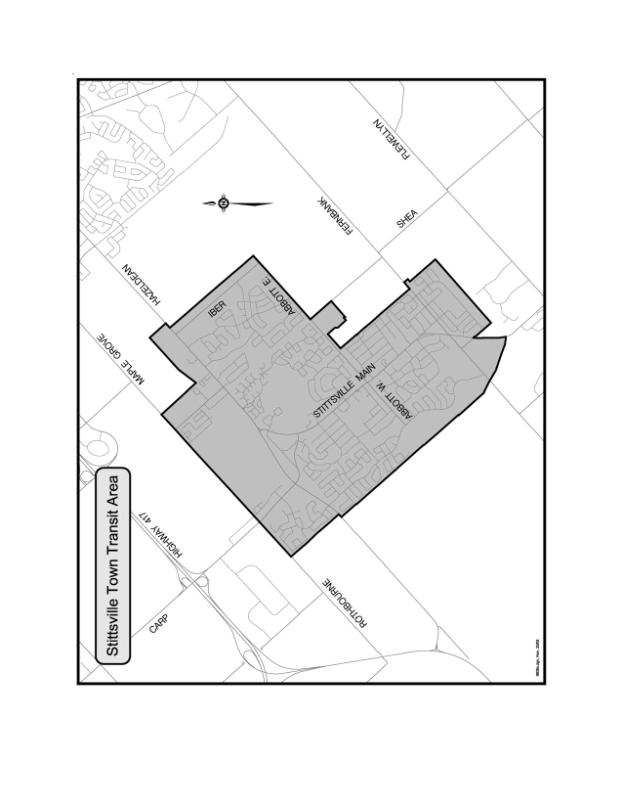

STITTSVILLE TOWN TRANSIT AREA DOCUMENT

4

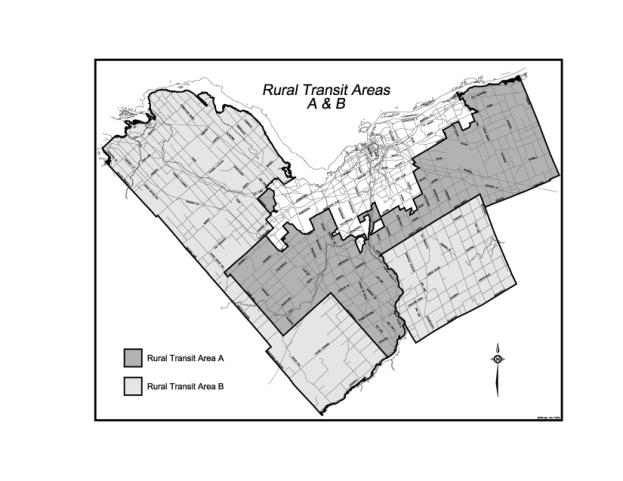

RURAL TRANSIT AREAS A AND B DOCUMENT

5

CHANGES IN TAX RATES WITH

CITY-WIDE SHARING

OF PARK AND RIDE

MAINTENANCE COSTS

DOCUMENT 6

Current Arrangement

|

|

2008 Weighted Assessment |

Levy |

Equivalent Rate |

Average House $279,000 |

|

Urban

Transit Area |

$97,192,882,443 |

$1,200,000 |

0.0012347% |

$3.44 |

|

Total |

$97,192,882,443 |

$1,200,000 |

0.0012347% |

$3.44 |

Recommended Arrangement

|

|

2008 Weighted Assessment |

Levy |

Equivalent Rate |

Average House $279,000 |

|

Urban

Transit Area |

$97,192,882,443 |

$1,064,582 |

0.001095% |

$3.06 |

|

Stittsville

Town Transit Area |

$2,297,085,257 |

$25,161 |

0.001095% |

$3.06 |

|

Rural

Transit Area A |

$4,938,216,748 |

$54,090 |

0.001095% |

$3.06 |

|

Rural

Transit Area B |

$5,127,932,376 |

$56,168 |

0.001095% |

$3.06 |

|

Total |

$109,556,116,824 |

$1,200,000 |

0.001095% |

$3.06 |

METHODS TO CHARGE

ADDITIONAL FEES FOR PARK AND

RIDE USERS FROM

OUTSIDE OTTAWA DOCUMENT

7

Staff do not recommend the application of different fees and charges for the use of the transit system depending on whether the home location of the customer is within or outside the City of Ottawa. While it is certainly true that customers living outside the city limits do not contribute to the cost of providing service through their property taxes, the benefits to city residents of having those travellers on the transit system are high. In addition, the possible methods that have been identified to accomplish the differentiation would variously be expensive, cumbersome, open to evasion, and would cause inconvenience for all transit customers.

Some possible methods are:

- Requiring all customers to use an electronic pass to enter the lots, controlled by automated gates. The passes would be sold to customers at transit sales offices or by mail (or would be in the future built into the smartcard system) and staff would check customers’ drivers’ licences to determine their home location before selling the pass or registering the customer into the automated system. This would have the disadvantages of requiring city residents to be issued passes, eliminating the possibility of spontaneous use of park and ride lots without buying a pass in advance, and increasing traffic congestion at the entrances to the lots. There would also be a capital cost to install gates and ongoing operating costs to sell the passes and maintain the gates. This option would allow evasion, as city residents could buy the passes and pass them along to friends or relatives living outside the city.

- Requiring all customers to display a pass in their cars. The passes would be sold to customers at transit sales offices, by mail, or on the web, and staff would check customers’ drivers’ licences to determine their home location before selling the pass or registering the customer into the automated system. Single-day passes could also be sold on the web or at pay-and-display machines within the lots. This would have the disadvantage of requiring city residents to be issued passes, and requiring single-day users of the lot to spend more time buying the pay-and-display pass and placing it in their car. There would also be a capital cost to install the pay-and-display machines and ongoing operating costs to inspect the passes each day, sell the passes, and maintain the machines. This option would allow evasion, as city residents could buy the passes and pass them along to friends or relatives living outside the city.

- Issuing all city residents with a pass or sticker for their cars and requiring people without a sticker to buy a pass or a pay-and-display ticket. The disadvantages would be as in the previous option. There would be an increased likelihood of evasion, as city residents who do not use the park and ride lots could easily pass their unused passes or stickers along to friends or relatives living outside the city. If the stickers were registered to specific licence plate numbers, this evasion could be reduced, but there would be an additional staff cost to check and prepare each individually.

- Installing an automated system as is used on some toll highways, to read either a prepaid transponder in each car or the licence plate on the car. Customers with cars registered inside the city would be able to park without charge, and customers from outside the city would be required to have a transponder. Customers with cars registered outside the city who did not have a transponder could be issued a parking violation ticket. There would be an extremely high capital cost to install such a system and a high ongoing staff cost to operate the system. This option would have the disadvantage of making it impossible for customers from outside the city to use the lots spontaneously without buying a transponder in advance.

The four options described here are not necessarily the only options possible, but they illustrate the range of issues that need to be considered. In each case, there are inconveniences caused to some or all customers who use the lots, and these would discourage transit use, by increasing complexity and reducing convenience. While there could be a revenue stream initiated from the fees to sell the passes or transponders, careful consideration would need to be given to ensure that the revenue is sufficient to offset both the ongoing operating costs and the loss of normal transit fare revenue that would result from the higher costs and the greater inconvenience. In addition, a comparison should be made as to whether the benefits to the city (primarily in advancing equity in transit contributions) exceed the drawbacks (primarily in reduced transit use and therefore increased auto use).